Accountability for business performance appears to be shifting irrevocably, albeit more slowly than that desired by the investor community. Historically, the performance of the enterprise rested at the feet of the CEO. Boards reported the performance of the business to shareholders and, on occasions, their broader stakeholder community. They rewarded or dismissed their CEOs on the basis of that performance. It was the CEO who was held accountable for performance by their board. However, over the last decade the expectations of shareholders and stakeholders have begun to change. Boards are increasingly being held responsible for business performance and legislation is now in place in most jurisdictions in the Anglosphere to enforce that outcome. The Sarbanes-Oxley Act is a case in point.

Accountability for business performance in New Zealand, by contrast, is both diffuse and confused. It is diffuse in the sense that the nexus for accountability is difficult to observe, mitigated by a raft of behaviours by corporate directors. And, it is confused because of the inconsistent findings by the judiciary where cases of failure have been brought before the courts. That accountability is yet to sit firmly with the board is not in question. That boards collectively, and directors individually, appear to use obfuscation, ignorance and deflection to counter the demands of accountability is, sadly, commonplace.

The aim of this article is to explore the behaviours of corporate boards in New Zealand where demonstrable failure has occurred. We conclude with the view that choices towards accountability are being made. However, both excuses and the shifting of scrutiny and blame away from the board collectively or directors individually are still far too common – more so in an environment where recovering confidence in the corporate governance community following the global financial crisis (GFC), and other tragedies, is best described as work in progress.

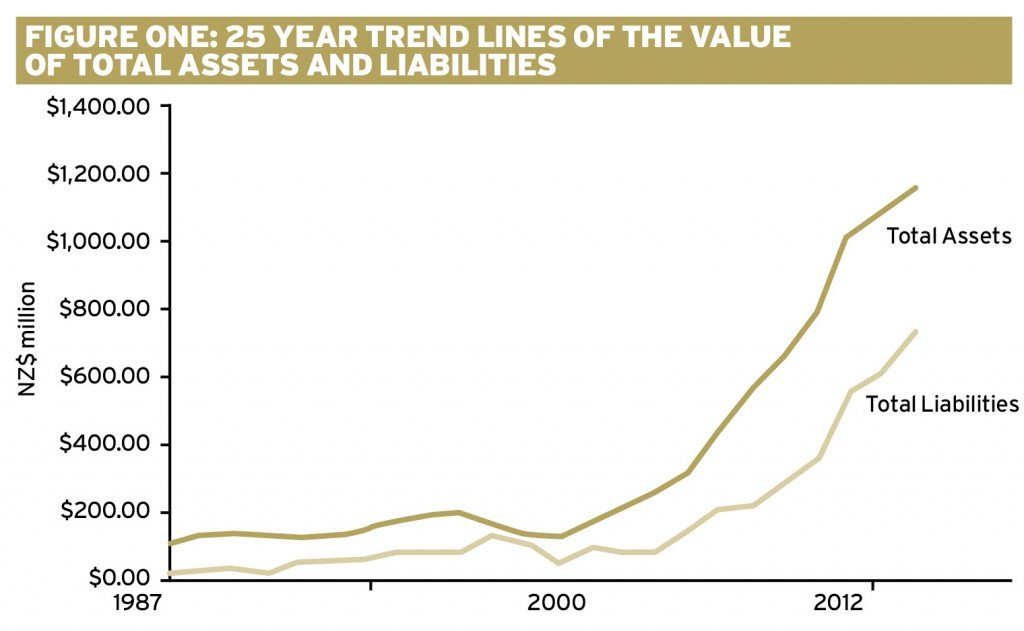

To illustrate the lack of accountability, consider the trend lines from a large business in Figures One and Two (below). The industry, business, and ownership are of no relevance to this discussion, save to say that the Y axis is in hundreds of millions of New Zealand dollars (NZ$1.00 = £0.487).

The trends shown in Figure One suggest that sustained asset growth has occurred over an extended period, accompanied by balance sheet growth, although most of the growth only emerges post-2000. The board(s) in this latter period can rightfully lay claim for success. However, this would be somewhat impetuous, because Figure Two paints a somewhat different picture of the very same business.

Over the same period as the balance sheet growth shown in Figure One, post-2000, there was a strong and sustained increase in annual sales turnover, albeit with increased volatility around the time of (and probably resulting from) the GFC. However, while asset growth occurred, there was little translation into EBIT growth, despite not inconsiderable effort applied to increasing sales turnover (Figure Two).

A detailed analysis of expenditure reveals sustained increasing trends, particularly across salaries, ‘consumption’ and, to a lesser extent, dividends. These expenses simply consumed the revenue gains made throughout the period. The company was expanding and growing, primarily through new borrowings. Expenditure continued to rise and little gain was made to EBIT (earnings before interest and taxes). The net result was insolvency.

In terms of accountability, the board laid fault everywhere but themselves. Blame was directed at external factors, market conditions, the GFC and so on. Management was kindly exonerated. However, at no stage does the board appear to have understood that the period of sustained post-2000 growth achieved little demonstrable impact on EBIT, or if it did, it appeared to have ignored the growing disparity. With the predictable exception of the impacts of the GFC, the analysis of all the annual reports from 1987 onwards did not reveal any concern that performance was less than satisfactory – yet suddenly the company was insolvent!

In another example – a different business in a different industry, but again a large scale enterprise – successive boards have supported management’s behaviours despite repeated failures, scandals and disrepute. At no stage has there been any published acceptance, or even acknowledgement, that something may have been wrong and something was being done about it. The board, on each occasion has been quick to distance itself from accountability. While this particular case now sits firmly with the Financial Markets Authority, due to the repeated lack of disclosure. The ongoing indifference, and possibly ineptitude, towards accountability appears to be having far reaching consequences among joint-venture partners, international markets and the shareholder base.

“Expectations of shareholders and stakeholders have begun to change. Boards are increasingly being held responsible for business performance”

These two examples are in stark contrast to the efforts of New Zealand’s governance administration to align responsibility and accountability for occupational safety and health, to which boards and directors appear to be responding both positively and effectively. This effort and the related legislative changes that have directly resulted from the deaths of 29 miners at the Pike River coal mine in 2010, New Zealand’s largest industrial accident (excluding the Mt. Erebus disaster in Antarctica in 1979) since the Strongman mine accident in 1967 which claimed 19 lives.

Our sense is that directors need to think very carefully before they are appointed and ensure they understand the duties they must fulfil having accepted that appointment: legal, ethical and moral. All directors have a duty of care and a duty of loyalty – to the company or to the shareholders (depending on the jurisdiction) and not just to themselves. This means that the director role is a servant role, of serving the best interests of the company/shareholders. In fulfilling these duties, directors need to be adequately informed and well-intentioned, lest the wool be pulled over their eyes by misinformation or they make decisions that are not consistent with their duties. They must also have the courage to admit, to accept, report and rectify mistakes, and reflect upon and learn from them. Furthermore, directors need to become far better at recognising and accepting their own failings and weaknesses, and addressing them, preferably before they get involved!

The role of the director bears a weighty responsibility, so directors need to take their appointments, and the accountability that goes with such appointments, seriously. Most do, but some, clearly, flout the boundaries of moral, ethical, and in some cases, legal acceptability. Directors need to be beyond reproach. Clear demarcations of what is acceptable – and what is not – need to be established. This may mean that the curious propensity to collect directorships, as some badge of honour it would seem, needs to be called into question by shareholders and by the profession’s body. That directors with six or more appointments have any hope of providing any more than a cursory contribution is beyond us. The challenge, of course, is holding directors to account for this level of performance, among peers, in the public domain and through any legal processes that may be required.

{kind=link}