Earlier this year, as proxy season was getting underway, circumstances seemed ripe for another banner year for ESG. ESG funds had grown considerably over the previous year and generated robust returns in-line with the market. ESG-focused shareholder proposals were set to reach a record high after getting unprecedented support from proxy advisors and institutional investors in 2021.

In the world of high-profile proxy battles, Carl Icahn’s activist campaign highlighting ethical food sourcing at McDonald’s was frequently compared in the media to Exxon, which had lost a proxy fight last year in a campaign based, in part, on climate change and energy transition.

Now halfway through the year, as proxy season winds down, some may think the tide has turned on ESG. ESG funds have seen net outflows recently, shareholder support for ESG proposals and proxy fights has significantly slowed since last year, and some noteworthy market participants have lashed out publicly at ESG, saving some choice words for the advancement of environmental, social and governance standards.[1]

Despite these setbacks, ESG is still a pervasive theme in the market today, and shareholder activists will likewise continue to try to leverage that momentum to their advantage. Companies that ignore this will risk not only alienating themselves from their shareholders but also making themselves more vulnerable to activism.

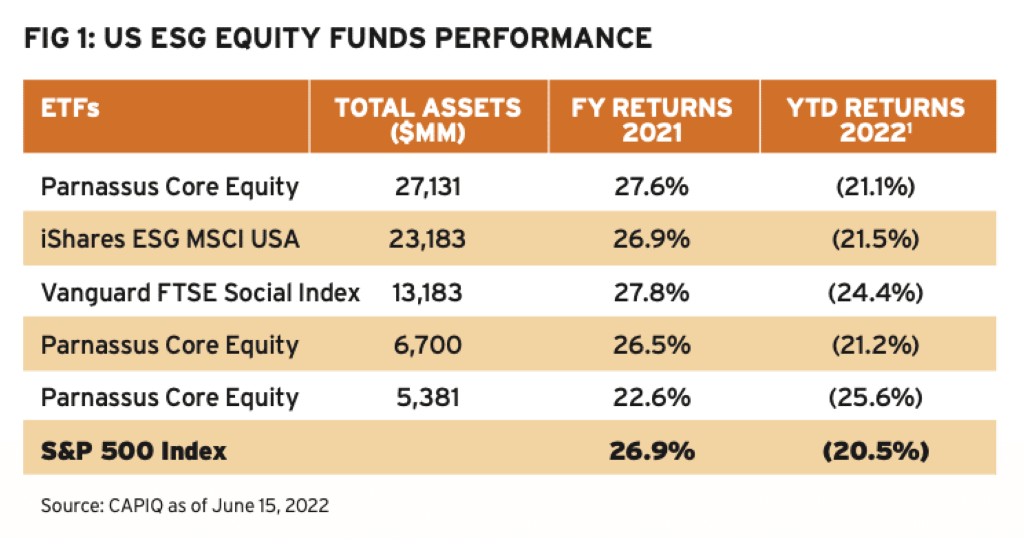

ESG Funds Performance

Last year, ESG fund returns were largely in-line with the market index but more recently have underperformed, as illustrated by five of the largest ESG equity funds versus the S&P 500 (see Fig 1).

This is not without good reason. A typical ESG portfolio might be relatively overweight in tech stocks, invest more in areas like clean tech where cash flows can be uncertain and deferred further into the future than other sectors, and be underweight in energy stocks. The current environment − defined by declines in tech stocks, increasing inflation and interest rates, and rising oil prices that boost energy companies’ valuations − would work directly against this type of portfolio allocation. Compound those challenges with a negative economic outlook and the impact it has on stock prices generally and you have a perfect storm for testing investors’ conviction in the ESG investment thesis.

For now, at least, this has not precipitated a mass exodus from ESG equity funds, although inflows of new capital slowed significantly in the first quarter.[2] To put that in perspective, inflows in the broader market dropped more dramatically over the same time period. More recently, Bloomberg reported that last month US ESG equity funds experienced their first net outflow of investment capital in over three years.[3] However, all US equity funds had a significant outflow just the month before (and a more modest one in January).[4]

These conditions have exposed some limitations to the degree that ESG investment strategies may track the broad market. While this goal might hold true in “normal” times, and prove true over the longer term, it appears less likely when significant market shocks impact sectors and asset classes in a different way. Once current conditions begin to stabilize and eventually normalize over the longer term, it is possible that ESG fund returns will recover. For the time being, it seems like at least part of the ESG investor community hopes to weather the storm.

E&S Shareholder Proposals

As of May, roughly 600 environmental and social (E&S) shareholder proposals had been submitted so far this proxy season, up about 20 per cent from last year and setting a new record.[5] In addition, new guidance from the SEC late last year has made it more difficult for companies to omit such proposals, and as a result, the percentage of E&S proposals that issuers successfully excluded from the shareholder meeting agenda is half of last year.[6],[7]

Although shareholders are voting on more E&S proposals than ever, the passage rate is only about half that of last year, so the number of proposals that have passed is actually down considerably in comparison with 2021.[8] However, we should not rush to assume that investors are showing less commitment to ESG objectives. Many proposals were farther- reaching than last year and voted on in a less amenable environment.

To spotlight the energy sector, carbon emissions and other climate- related proposals in 2021 called for setting long-term commitments toward carbon neutrality. Today’s proposals go further, calling for more specific short- and intermediate-term targets for reducing emissions. A recent BlackRock bulletin acknowledged that these proposals were more prescriptive than last year, and were being considered during a more uncertain time for energy prices and stability, saying therefore it would support fewer such proposals this year.[9]Although voting data won’t be widely available until later this year, other institutions seem to be taking a similar, more balanced approach rather than adopting a wholesale change of ESG values.

Nonetheless, a substantial number of E&S proposals have passed in 2022 and many others came very close. Several climate-related proposals received over 30 or 40 per cent shareholder support, with at least one coming within a few percentage points of passing.[10] In the social category, shareholder proposals calling for social equity audits, where companies assess the degree to which their business has an uneven impact on different communities, passed at some companies but narrowly failed at some others. These types of proposals may well be re-submitted and voted on again next year, and in a more stable political and macroeconomic climate, might pass.

ESG Proxy Fights: Carl Icahn vs McDonald’s and Kroger

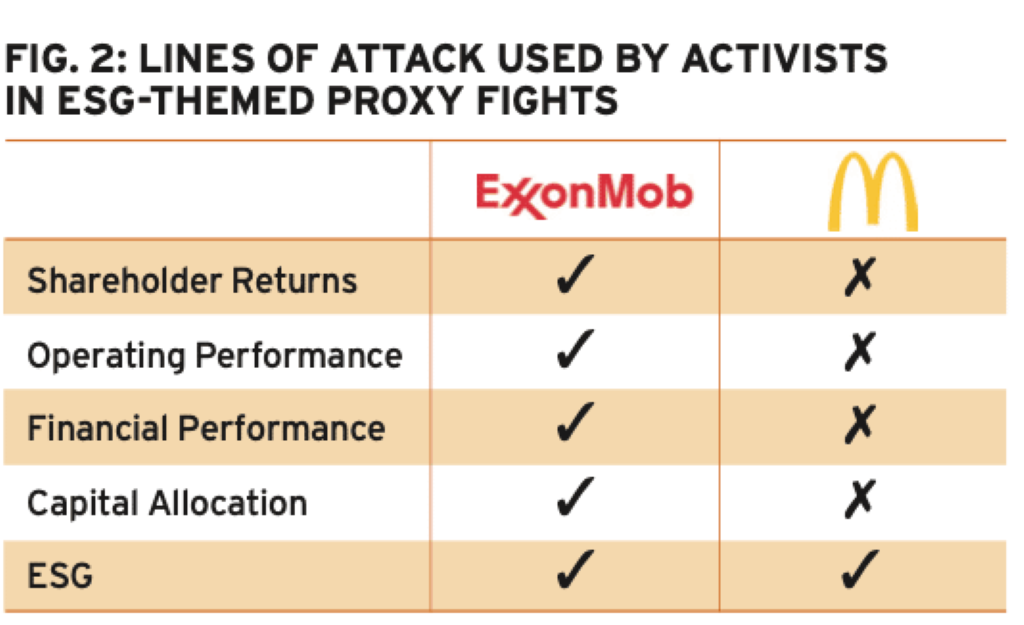

In its campaign for board seats last year at Exxon, Engine No.1 focused as much on traditional activist lines of attack as it did on issues around climate change and energy transition. Topics such as shareholder returns, capital allocation, business and financial performance, and board composition and oversight were all part of the activist’s thesis and prominent themes in its investor communications to proxy advisors and Exxon shareholders.[11]

In fact, proxy advisor Institutional Shareholder Services (ISS), in its recommendation for three of the activist’s nominees (who were ultimately elected), found operating performance and capital allocation to be core issues its conclusions were based on, although in part intertwined with energy transition and sustainability.[12] Memos subsequently released by Exxon’s top three shareholders Vanguard, BlackRock and State Street outlining their voting rationales, described a similar combination of considerations.[13] In short, Engine No.1’s campaign relied on still establishing the typical core elements of an activist campaign that one customarily sees, although connected to ESG.

By contrast, Carl Icahn, in his campaigns this year against McDonald’s and Kroger, tested the boundaries a bit further and relied exclusively on ESG-focused arguments around ethical sourcing and treatment of animals, without addressing the other key, more fundamental areas of vulnerability. In the end, Icahn did not win the support of the proxy advisors or McDonald’s shareholders. Shortly thereafter, Icahn also withdrew his campaign at Kroger. While these are different companies from Exxon, in different industries, and different ESG issues were involved, Icahn himself concluded that:

“My campaigns concerning McDonald’s and Kroger were different from most of the companies in which I have been an activist, in that both of these companies are well-performing, financially speaking… It is clear that shareholders, even if they are concerned about the issues we highlighted, are not willing to change the board configuration if a company is performing well financially.”[14]

However, while these campaigns may clarify the limitation on the degree to which an activist can depend on ESG-related arguments to win board seats, it doesn’t change the fact, proven at Exxon, that ESG can still be a very effective component of an activist campaign and media platform. As a result, companies going forward must continue to include ESG in the criteria for assessing their overall vulnerability to activism. (See Fig 2).

Being Prepared

While the first half of 2022 may have revealed some limitations of ESG investing and activism, market and economic conditions that may have worked against ESG funds so far this year will normalise over time, and activists will adapt their tactics to the lessons learned this year. As the institutional investor community continues to incorporate ESG into their decision-making and voting behaviour, activists will likewise continue to try to harness this trend to have their own goals met. Therefore, companies should at a minimum be aware of the following things when thinking about ESG:

■ How the market perceives you on ESG

Today there is an ever-growing alphabet soup of ESG ratings and rankings in the market, with a low correlation among them, meaning they can produce widely divergent results, which reflects the array of methodologies, inputs and scoring conventions used.[15] Critics also complain of arbitrary or inaccurate analysis and the inadequacy of trying to reduce several complicated and potentially unrelated factors to a single letter score.[16]

Despite any shortcomings, the fact is that ESG ratings data has become widely-used in the market. ESG funds use them to build their portfolios, governance teams at large institutional investors rely on them for data and analysis, and activists who focus on ESG incorporate ratings into their public campaign materials (e.g., the activist’s proxy fight investor presentations at Exxon, McDonald’s, and Hunstman Corp.)[17] It’s important for companies to be aware of which ESG ratings matter and are relevant to their shareholders and sector, how they stack up versus peers and what the drivers are, and how to mitigate any apparent deficiencies. Oftentimes areas where a company looks like a negative outlier can be readily addressed with the help of an advisor that understands and can deconstruct the ratings, their methodologies and drivers, not just regurgitate a summary of the scores, to implement an effective remediation strategy.

■ What are the ESG issues your shareholders care about?

As part of companies’ regular IR and shareholder engagement programs, they should offer to discuss ESG goals and how they tie into the long-term business strategy so you can exchange ideas and hear and understand shareholders’ views. While you cannot please every shareholder constituency all of the time, you have to decide where to strike the right balance to do right for your shareholders as a whole and protect their long-term value. You simply cannot do that without first understanding their positions, even if you ultimately may agree to disagree with some. For key shareholders you may not speak to regularly, many larger institutions publicly disclose their policies and voting guidelines on ESG issues and their current priorities, and update these regularly. Lastly, look into how large shareholders have voted previously on shareholder proposals that may impact your sector.

■ How ESG might impact your vulnerability to activism

While ESG may not be a primary driver of activist vulnerability, it can certainly be a powerful springboard for an activist’s campaign, given the attention it gets from the institutional investor community, the proxy advisors and the media. ESG could be a component of the activist’s thesis for value creation, or just a wedge issue used by the activist to try to undermine confidence in management and depict the board as misaligned with shareholders. This can especially be true where an activist can link underperformance in the minds of shareholders with the ESG priorities those shareholders have committed to publicly.

Companies should therefore understand how their ESG profile may exacerbate other areas of activism vulnerability, such as business and financial performance, capital allocation, and long-term competitive strategy and how to execute it. As with the ratings, often apparent weaknesses can be effectively addressed well in advance of when an activist shows up.

An Ounce of Prevention

The steps outlined above are most beneficial when undertaken ‘on a clear day’. Companies will be able to make holistically better decisions for all stakeholders and set an optimal course for the business when the information gathering, analysis and planning are done before a potentially heated situation with a shareholder arises. In addition, companies will be better prepared to respond quickly and effectively when these incidents do occur or may be able to avoid the cost and distraction of one altogether.

Footnotes:

[1] See Stempel, Jonathan. “Berkshire Shareholders Reject Climate Change, Diversity Proposals that Buffett Opposed.” Reuters. May 1, 2021, available here; Kelley, Trista. “Peter Thiel Leads Bitcoin Backers Blasting ESG ‘Hate Factory’.” Financial News. Apr 8, 2022, available here. Prang, Allison. “Elon Musk Calls ESG ‘An Outrageous Scam’ After Tesla Was Removed From Index.” Wall Street Journal. May 18, 2022, available here.

[2] Stankiewicz, Alyssa. “US Sustainable Fund Flows Slid in First-Quarter.” Morningstar. May 2, 2022, available here.

[3] Forte, Peyton. “ESG Equity Funds Experienced Record Month Of Outflows In May.” Bloomberg. Jun 1, 2022, available here.

[4] Lynch, Katherine. “U.S. Stocks Funds See Inflows In May Despite Market Turmoil.” June 14, 2022, available here.

[5] Layne, Rachel. “Climate Shareholder Resolutions Flood into Proxy Season for a Record Year.” Fortune. June 6, 2022, available here.

[6] “Shareholders Up Climate, Social Demands After SEC Policy Shift.” Bloomberg Law. April 4, 2022, available here.

[7] See Georgeson. “An Early Look At the 2021 Proxy Season.” July 15, 2021, available here.

[8] Bantz, Phillip. “ESG Shareholder proposals Spike In 2022 But Garner ‘Muted’ Support.” June 1, 2022, available here.

[9] BlackRock, Inc. “2022 Climate-Related Shareholder Proposals More Prescriptive Than 2021.” May 2022, available here.

[10] Source: Proxy Insight.

[11] See e.g., Engine No. 1’s shareholder communications available online here.

[12] Herbst-Bayliss, Svea. “Exxon Under Pressure As ISS Backs Engine No. 1 Nominees In Board Fight.” May 14, 2021, available here.

[13] BlackRock, Inc. “Vote Bulletin: ExxonMobil Corporation.” May 2021, available here; State Street Global Advisor. “Vote Bulletin: ExxonMobil Corporation.” May 2021, available here; and The Vanguard Group. “Vote Bulletin: ExxonMobil Corporation.” May 2021, available here.

[14] Icahn’s letter to McDonald’s and Kroger shareholders available here.

[15] Berg, Florian, Koelbel, Julian., & Rigobon, Roberto. “Aggregate Confusion: The Divergence of ESG Ratings.” August 20, 2019, available here.

[16] See, e.g., Pham, Lisa. “ESG Backlash Has Fund Clients Demanding Proof It Works.” May 31, 2022, available here.

activism.){kind=link}